A cooperative society is one of the most powerful and legally recognized business models in the world. In Nigeria and across Africa, cooperative societies help people pool resources, access affordable capital, and build wealth together

Whether through ajo, esusu, or modern investment groups, the instinct to collaborate remains strong. Cooperatives are often mistaken for outdated unions or savings clubs, but in reality they are sophisticated, legally protected enterprises that can scale into multi‑billion naira organizations.

This guide will explain what a cooperative is, how it works, the types available, and the benefits. So you can decide the right structure for your community or business.

Cooperative Societies Are Bigger Than Most People Realize

One of the biggest misconceptions about cooperative societies is that they are small community savings groups with limited impact. In reality, cooperatives are among the largest and most resilient economic institutions in the world.

Globally, they serve over one billion members and generate trillions of dollars annually across industries like banking, agriculture, insurance, retail, housing, healthcare, and manufacturing.

Far from being niche, cooperatives have become one of the most enduring systems for building wealth, expanding financial inclusion, and giving ordinary people collective ownership of the institutions they rely on.

Some of the world’s most successful organizations thrive precisely because they are cooperatives.

Global Cooperative Societies Success Stories

| Cooperatives | Success Stories |

| Rabobank (Netherlands) | It is a financial cooperative that began as farmer‑owned credit unions and has grown into one of the world’s largest cooperative banking institutions. |

| The Co-operators (Canada) | A member-owned insurance cooperative that has grown into one of Canada’s leading insurance providers, offering property, casualty, life, and investment products while remaining cooperative-owned. |

| Coop Group (Switzerland) | One of Switzerland’s largest retail organizations, owned by cooperative members and operating supermarkets, pharmacies, restaurants, and wholesale businesses across the country. |

| Co-op City (New York, USA) | One of the largest housing cooperatives in the world, providing affordable housing to tens of thousands of residents through collective ownership and governance. |

| Fonterra (New Zealand) | Owned by thousands of dairy farmers, Fonterra is one of the world’s largest dairy exporters and a major player in the global food industry. It demonstrates how farmers can achieve international scale through cooperative ownership. |

What is a Cooperative Society?

| 📌 Quick Answer (AEO Block)A cooperative society is a member-owned, democratically controlled organization where individuals voluntarily pool their resources to meet shared economic, social, or cultural needs. Unlike traditional corporations that exist to maximize returns for outside investors, a cooperative exists solely to provide mutual benefits, manage shared financial risks, and give its members affordable access to capital, goods, or services all under the principle that every member has an equal voice, regardless of wealth. |

Let’s go deeper than the definition.

The word “cooperative” comes from the Latin “cooperari” to work together. And that is precisely what it is: a structured, legal framework for working together toward a shared goal.

In Nigeria, a cooperative society is formally recognized under the Co-operative Societies Act (Cap C36, Laws of the Federation of Nigeria 2004), and is registered not with the Corporate Affairs Commission (CAC) the way a limited liability company is, but with the relevant State Ministry of Commerce and Cooperatives in the state where the group operates.

The most important thing to understand is who this structure was designed to protect: the ordinary member.

Section 1: How a Cooperative Society Works

To understand a cooperative, you have to look at who holds the keys. In a standard business, money buys power — whoever owns the most shares controls the most decisions. In a cooperative, participation buys power.

Cooperatives around the world operate based on seven internationally recognized principles established by the International Co-operative Alliance (ICA), the global body representing cooperative movements across more than 100 countries.

These principles — including democratic member control, member economic participation, autonomy and independence, education and training, cooperation among cooperatives, and concern for community — form the foundation of modern cooperative governance worldwide.

In other words, the rules that guide a cooperative society in Nigeria are built on the same principles that guide cooperative banks in Europe, agricultural cooperatives in Latin America, and worker-owned enterprises in North America.

This global consistency is one reason the cooperative model has remained relevant for more than a century.

1. Capital Pooling — Financial Strength in Numbers

Starting a business, purchasing equipment, or accessing a market as a single individual is expensive and risky. A cooperative solves this by allowing members to buy shares or contribute regular savings into a shared fund.

Imagine 200 market traders in Lagos each contributing ₦5,000 per month. In one year, that pool holds ₦12,000,000. That capital can be used to:

- Issue low-interest loans to members who need working capital

- Purchase raw materials or stock in bulk at wholesale prices

- Invest in shared infrastructure — like a cold room, warehouse, or logistics vehicle

- Build a reserve fund that protects the group against unexpected financial shocks

This is the fundamental power of a cooperative: collective financial muscle. It allows ordinary people to access resources and opportunities that were previously only available to wealthy individuals or large corporations.

2. Democratic Member Control — One Member, One Vote

This principle is the ultimate trust shield, and it is what makes cooperatives fundamentally different from every other business structure.

In a traditional limited liability company, if an investor owns 51% of the shares, they completely control the company. They can outvote every other person combined. They can change the mission, fire the management, redirect the funds, or sell the company to a stranger and there is nothing you can do about it.

In a cooperative, governance is entirely democratic. No matter how much money you have or how many shares you hold, one member equals one vote. Always. A wealthy outsider cannot swoop in, buy up influence, and alter the direction of your community group. This rule is non-negotiable and is protected by law.

| 💡 Why This Matters in Nigeria Given the rise of fraudulent investment schemes and digital savings platforms that collapsed and left members stranded, the democratic governance structure of a registered cooperative creates a critical layer of accountability. Leadership is elected — and can be voted out — by the members themselves. |

3. Surplus Allocation — True Profit Sharing

At the end of each financial year, after the cooperative pays all its operating costs: staff salaries, office rent, loan defaults, administrative expenses. it is left with what is called a surplus (the cooperative word for profit).

Here is where cooperatives become truly different. It routes the money is returned directly to the members through a patronage refund. It is profit-sharing calculated based on how actively you used the cooperative’s services throughout the year not how much money you originally put in.

If you borrowed more loans, bought more cooperative stock, or transacted more with the cooperative than another member, you receive a proportionally larger share of the surplus. Participation is rewarded. Passive membership earns less. This structure incentivizes members to actually use and grow the cooperative, which benefits everyone.

Section 2: Main Types of Cooperative Societies

Not all cooperatives are built the same. Depending on what a community needs — financial access, agricultural marketing, housing, or consumer goods — cooperatives take on entirely different structural forms. Across the world, and particularly in Nigeria, five major models dominate the landscape:

1. Thrift & Credit Cooperative Societies (CTCS) — The Financial Backbone

This is, by far, the most common type of cooperative in Nigeria. A Thrift and Credit Cooperative Society — often called a SACCO (Savings and Credit Co-operative Society) in East Africa — operates as a community-owned alternative to traditional banking.

Members contribute a fixed monthly savings amount (the thrift). The cooperative pools this capital and uses it to issue low-interest loans to members — without the aggressive collateral requirements or sky-high interest rates of commercial banks. Instead of qualifying based on your credit score or property title deeds, you qualify based on your contribution history and membership standing.

Across Nigeria, CTCS cooperatives are found in:

- Workplaces — civil servants, hospital workers, teachers, and factory staff forming department-level thrift groups

- Markets — traders pooling funds for working capital and bulk purchasing

- Churches and mosques — congregational savings groups formalized under cooperative law

- Professional networks — tech workers, lawyers, accountants forming investment-focused SACCOs

| 🌍 Real African ExampleStima DT SACCO in Kenya, serving energy sector workers, has grown from a small departmental savings group to managing billions of shillings in assets — all while keeping interest rates on member loans at a fraction of commercial bank rates. Similar workplace cooperatives are the fastest-growing cooperative category across Nigeria today. |

2. Agricultural Cooperatives — Strength at the Farm Gate

Smallholder farmers across Nigeria face two devastating problems: the high cost of farm inputs (fertilizer, seeds, equipment) and weak bargaining power when selling their produce to middlemen and aggregators.

An agricultural cooperative society solves both. By pooling demand, a group of farmers can purchase inputs at wholesale prices, dramatically cutting production costs. By pooling supply, they can negotiate collective selling prices directly with major buyers, processors, or export companies — cutting out the middleman entirely.

Agricultural cooperative societies are particularly strong in:

- Cocoa farming communities in Ondo, Osun, and Ekiti states

- Cassava and yam cultivation in Benue and Kogi states

- Rice farming cooperatives supported by the CBN Anchor Borrowers Programme

- Sesame seed and soybean production cooperatives in Nassarawa State

| 🌍 Real African ExampleThe Okyeman Cocoa Farmers Co-operative in Ghana is a landmark case study. By organizing smallholder farmers into a cooperative structure, members were able to achieve Fairtrade certification, access global export markets directly, and earn premiums that individual farmers could never have negotiated alone. |

3. Consumer Cooperatives — Buy Together, Save Together

A consumer cooperative is formed when a group of people come together to purchase goods or services in bulk at significantly reduced prices. The savings from bulk purchasing are passed directly to the members — not kept as corporate profit.

Think of it this way: a single household buying cement, roofing sheets, or cooking gas pays full retail price. A consumer cooperative society of 500 households buying those same products directly from the manufacturer or distributor commands a wholesale discount that individual buyers could never access. In Nigeria, you see this model among:

- Market trader associations pooling stock purchases to reduce per-unit costs

- Housing cooperative societies buying building materials collectively

- Estate resident associations collectively procuring diesel, water, and security services

4. Housing Cooperatives — Collective Pathways to Homeownership

With property prices in Lagos, Abuja, and other major cities now completely out of reach for most Nigerians, housing cooperatives are gaining significant traction. Members pool contributions over a set period toward a shared housing fund, which is then used to purchase land, develop estate units, or access mortgage financing at group rates.

The Federal Mortgage Bank of Nigeria (FMBN) and the National Housing Fund (NHF) both have provisions specifically designed to work with registered housing cooperative societies, making it one of the most practical pathways to homeownership for middle-income Nigerians.

5. Worker Cooperatives — Own the Business You Work In

In a worker cooperative, the employees are the owners. Every worker is a member-owner who shares in both the decision-making and the financial surplus generated by the enterprise. This model eliminates the traditional adversarial relationship between employer and employee — because they are the same people.

In Nigeria, worker cooperative societies are common among artisan groups — tailors, carpenters, welders, and mechanics — who pool tools, share workshop space, and collectively bid for large contracts that individual craftspeople could never handle alone.

| 🌍 Global Benchmark Mondragon Corporation in Spain — one of the world’s 10 largest companies by revenue — operates entirely as a federation of worker cooperatives, employing over 80,000 worker-owners across manufacturing, finance, retail, and technology. |

Section 3: Benefits of Joining a Cooperative Society

Understanding what a cooperative is and how it works is the foundation. But the question that truly matters is: why should you — a busy Nigerian professional, entrepreneur, farmer, or trader — actually bother?

Here are the five core benefits that make the cooperative model one of the most powerful tools for financial empowerment available to ordinary Nigerians today:

1. Shared Financial Risk — No Single Person Bears the Burden

When a single entrepreneur takes out a bank loan at 28% per annum to fund a business, a market crash, a delayed government contract, or a naira devaluation can wipe out their personal livelihood overnight. They carry the entire weight of that risk alone.

In a cooperative, risk is distributed across the entire member network. If one member defaults on a loan, the cooperative’s reserve fund absorbs the shock — not the other members’ personal savings.

2. Access to Affordable Capital — Loans Without the Predatory Terms

Commercial banks in Nigeria currently offer personal and SME loans at interest rates ranging from 25% to 35% per annum. Microfinance institutions are often worse. For a small business owner, these terms can be financially ruinous.

Cooperative thrift societies typically offer member loans at 1% to 2% per month flat — equivalent to 12% to 24% per annum — with no collateral requirements beyond your membership contribution history. For a member with a strong savings track record, a cooperative loan can be the difference between surviving a cash flow gap and shutting down a business.

3. Collective Bargaining Power — The Cooperative Discount

One of the most immediate and tangible benefits of cooperative membership is price power through scale. An individual artisan buying construction materials pays retail. A cooperative of 300 artisans buying those same materials orders at a volume that commands wholesale pricing, bulk delivery, and extended credit terms from suppliers — benefits that would be completely inaccessible to any single member acting alone.

This applies across sectors: agricultural inputs, consumer goods, real estate, medical supplies, and insurance premiums. The larger and more active the cooperative, the more negotiating leverage it holds.

4. Democratic Transparency — Your Money, Your Voice

In a traditional company, you can invest your savings and have absolutely no visibility into how that money is being managed. You have no vote. There’s no seat for you at the table. Dependence falls entirely on the goodwill and competence of management.

In a registered cooperative, you are legally entitled to audited annual financial statements presented at the Annual General Meeting (AGM), which every registered cooperative is legally required to hold. You can question the committee, challenge line items, and — if you are unsatisfied — vote out the management and elect new leadership on the spot.

5. Community Wealth Building — Capital Stays Local

When a Nigerian takes a personal loan from a commercial bank, the interest payments flow upward — to bank shareholders, foreign investors, and corporate headquarters. The money leaves the community.

When a member of a thrift cooperative borrows money, the interest they pay stays within the cooperative — it becomes part of the surplus that is redistributed to all members at year-end. The wealth circulates within the community, compounding over time into a growing financial ecosystem that benefits every member.

The global impact of this model is difficult to overstate. According to international cooperative research, the world’s largest cooperatives generate trillions of dollars in annual turnover. This is one reason why organizations such as the United Nations recognize cooperatives as important vehicles for sustainable economic development, financial inclusion, and community wealth creation.

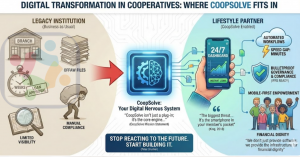

If Cooperative Societies Are So Powerful, Why Do So Many Struggle?

For more than 180 years, cooperatives have helped communities pool resources, access affordable capital, and build wealth together. The model itself is remarkably resilient.

Yet many cooperatives fail for reasons that have nothing to do with the cooperative structure itself. The challenge is often operational.

When Growth Outpaces Manual Processes

As a cooperative society grows, administration becomes increasingly complex. Savings records live in spreadsheets. Loan approvals become difficult to track. Financial reports take weeks or months to prepare. Members struggle to verify balances. Committee members spend countless hours reconciling spreadsheets and paper records. Institutional knowledge sits with one or two trusted individuals.

Over time, trust is not lost because money disappeared. Members can no longer clearly see where contributions are going, how loans are being managed, or whether decisions are being applied fairly and consistently.

With 20 members, a cooperative can survive on manual processes.

At 200 members, it requires systems.

Once it reaches 2,000 members, infrastructure becomes essential.

This reality is what led to the creation of CoopSolve.

CoopSolve was built around a simple belief: cooperative leaders should spend less time chasing records and more time serving members.

CoopSolve helps cooperative societies move beyond manual administration and fragmented record-keeping by providing a centralized platform for member management, savings tracking, loan administration, approvals, reporting, and governance workflows.

Instead of relying on paper ledgers, disconnected spreadsheets, or endless chats, cooperative leaders can manage operations from a single platform while members gain visibility into their savings, loans, contributions, and cooperative activities. The result is greater transparency, stronger accountability, and increased member trust.

The goal is not to change the cooperative model.

The goal is to help cooperatives scale without losing the trust that made them successful in the first place.

What Comes Next?

You now have a clear understanding of what a cooperative society is, how it works, and why it remains one of the world’s most effective models for collective wealth creation. From local savings groups to global institutions like Rabobank, Fonterra, Coop Group, and Co-op City, cooperatives have proven that ordinary people can achieve extraordinary results when they pool resources, share responsibility, and govern democratically.

But successful cooperative societies don’t happen by accident. They are built on strong governance, transparency, and trust.

If you’re already managing a cooperative—or planning to start one—having the right systems in place can make all the difference. CoopSolve helps cooperative societies streamline member management, track savings and loans, improve transparency, and simplify day-to-day operations from a single platform.

Want to see how it works? Request a demo and our team will walk you through the platform, answer your questions, and show how CoopSolve can help your cooperative society.

Ready to Digitize Your Cooperative?

CoopSolve helps cooperative societies automate member management, contributions, loans, reporting and compliance from a single platform.

Book a Demo